The SpaceX IPO Playbook: How Elon Musk Is Gaming the Public Markets

SpaceX targets the biggest IPO in history at $1.75 trillion. Inside the astrological timing, xAI merger risks, low-float manipulation, and why the math doesn't add up.

The Astronomical (and Astrological) Event of the Century

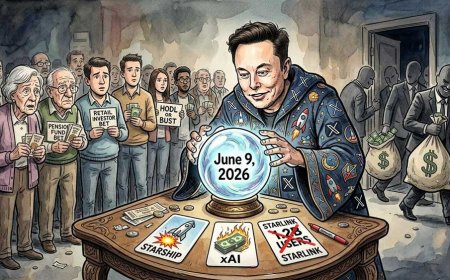

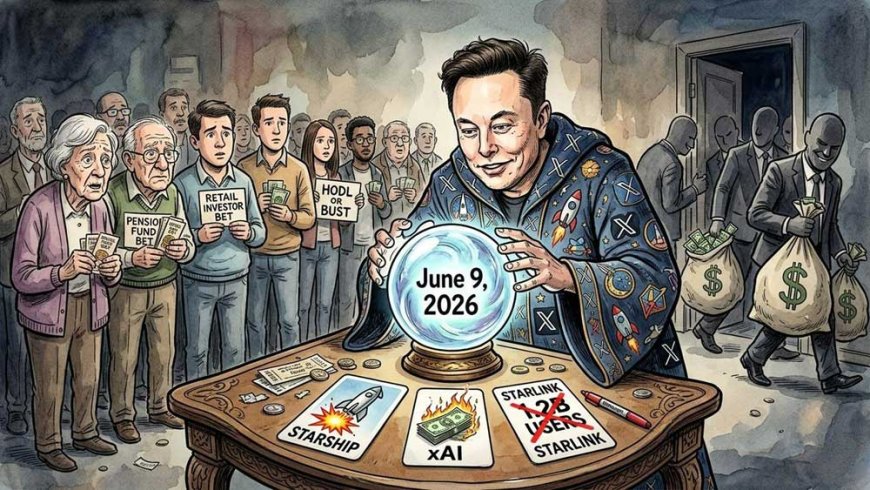

SpaceX (Shartify Trust Rank (Pre-IPO): 6.67) is preparing to execute the largest stock market debut in history, targeting a valuation of $1.75 trillion that would surpass Saudi Aramco's $29 billion record set in 2019. The chosen date? June 2026, ideally June 8th or 9th, when Jupiter and Venus will align in the sky in a rare conjunction visible for the first time in three years, followed days later by Mercury's alignment.

June 8th, in particular, coincides with the infamous "69" — a date echoing Elon Musk's numerological obsession with the numbers 420 and 69, which emerged in 2018 when he jokingly tweeted about taking Tesla private at $420 per share. To complete the picture, Musk will turn 55 on June 28, 2026, potentially becoming the first trillionaire in history if SpaceX reaches its target valuation.

According to sources cited by the Financial Times, it is Musk himself pushing for this "auspicious" timing. A choice that, beyond astrological implications, hides cold financial logic: the race to secure limited capital before OpenAI and Anthropic exhaust available demand in public markets.

The xAI Merger: When the Rocket Meets the "Money Furnace"

Months before the IPO, Musk decided to merge SpaceX with xAI, his artificial intelligence startup, in a deal valuing xAI at $250 billion and the combined entity at approximately $1.25 trillion. This represents the largest acquisition of a private company in history.

The problem? xAI is a "money furnace" burning through $1 billion per month to build its data centers, generating just $120 million in revenue in the first nine months of 2025. In other words, xAI spends its entire annual revenue every six days.

The merger also includes X (formerly Twitter), the social platform acquired by Musk for $44 billion in 2022 and subsequently transferred to xAI. SpaceX investors will thus become de facto owners of the world's 17th largest social network, a business experiencing persistent user and advertiser exodus since Musk's 2022 acquisition.

Musk justifies the deal with a science-fiction vision: the necessity of building orbital data centers to "extend the light of consciousness to the stars," harnessing solar energy in space and bypassing terrestrial constraints of land, power, and cooling. A proposal reminiscent of the controversial SolarCity merger of 2016, when Musk used Tesla's balance sheet to bail out a struggling solar company he also happened to own.

Space Data Centers: Physics vs. Musk's Ambition

Musk's xAI merger pitch hinges on "Sentient Suns"—a swarm of one million satellites acting as orbital data centers, tapping endless solar power while dodging Earth's limits on land, electricity, and cooling. Yet this clashes head-on with harsh physics and engineering barriers.

Heat Dissipation in the Void Earth data centers rely on fans, air, or water to whisk away heat via convection. Space offers no such luxury in its vacuum; satellites must radiate infrared heat through giant fins alone. A recent demo by a startup—a fridge-sized satellite with an Nvidia H100—trained a small AI model on Shakespeare but throttled to a crawl from overheating, unable to run continuously.[web:previous context] The upgraded 2026 version deploys the largest radiator array since the ISS to power just a few chips, hinting at absurdity: orbiting supercomputers demand hardware on par with our priciest megastructures, while Musk eyes a million-satellite fleet.

Scale's Breaking Point Musk's gigawatt vision per satellite would require solar arrays and radiators spanning roughly four kilometers—think 40 soccer fields per unit, lofted into fragile orbit. In LEO's debris-filled chaos (over 36,500 tracked objects whizzing at bullet speeds), these behemoths become sitting ducks for collisions, demanding constant repairs amid launch costs that dwarf terrestrial alternatives.

The 1.2 Billion User Hypothesis: A Total Addressable Market Analysis

However, this estimate contains a fundamental flaw in the Total Addressable Market (TAM) concept. Starlink's current pricing model—approximately $120 per month for residential service plus $599-$2,500 in hardware costs—immediately excludes the vast majority of global consumers. According to World Bank data, over 3.4 billion people live on less than $6.85 per day (the upper poverty line for lower-middle-income countries), while the global median household income sits around $10,000 annually. A service costing $1,440 per year plus substantial upfront hardware investment is simply inaccessible to most of the world's population.

Even among wealthier demographics, infrastructure competition severely limits Starlink's addressable market. In OECD countries, representing roughly 1.3 billion people, over 85% of households already have access to wired broadband offering superior latency, unlimited data, and lower costs. Starlink's satellite technology, while revolutionary for remote areas, suffers from inherent limitations: network congestion during peak hours, weather sensitivity, and the physical requirement for unobstructed sky view—making it impractical for dense urban environments where most affluent consumers actually live.

Geographic constraints further shrink the realistic market. Starlink requires ground stations within approximately 1,000 kilometers of user terminals, and regulatory approval varies dramatically by jurisdiction. Countries representing nearly 40% of global population—including China, India, Russia, and much of the Middle East—either prohibit Starlink entirely or impose severe operational restrictions for national security reasons.

Realistically, Starlink's serviceable addressable market (SAM) likely comprises 25-35 million households globally: remote rural properties in wealthy nations, maritime and aviation sectors, military applications, and isolated industrial operations. Expecting growth from 10 million current subscribers to 1.2 billion users—a 120-fold increase—requires assuming Starlink could capture subscribers in markets where it faces regulatory barriers, price inaccessibility, or superior terrestrial alternatives.

The marginal economics already reveal this tension. In 2024, Starlink reached 9.2 million subscribers (over 50% above Morgan Stanley's 6 million projection), yet generated $16 billion in revenue versus the projected $19 billion. The revenue shortfall despite subscriber overperformance indicates aggressive discounting, promotional pricing, and market share capture in lower-yield segments—classic signs of a business approaching its addressable ceiling rather than experiencing unconstrained exponential growth.

The Low Float Trap and Index Manipulation

The most disturbing element of the SpaceX IPO concerns its offering strategy. According to financial press, SpaceX will release only 5-10% of total shares, creating artificial scarcity that could generate price "squeezing" before the opening bell even rings.

But there's more. SpaceX has made accelerated inclusion in the Nasdaq 100 after just 15 trading days a necessary condition for listing, bypassing the one-year "seasoning" required for all other companies. S&P Dow Jones Indices is also reportedly considering historic rule changes to fast-track SpaceX into the S&P 500.

The most controversial mechanism is the 5x float multiplier: if SpaceX releases only 5% of shares at a $1.75 trillion valuation, passive funds would treat the stock as if it had a float of $437 billion (5 x $87 billion actual), forcing ETFs like Invesco QQQ to chase the price upward regardless of market conditions.

As veteran fund manager George Noble observed, this mechanism transforms every pension fund into "exit liquidity for SpaceX insiders" — citizens' retirement savings will be forcibly diverted to buy an artificially inflated stock, precisely as early investors prepare to sell when lock-up periods expire (typically 90-180 days).

We've seen this movie before: when Tesla was added to the S&P 500 in December 2020 after a massive price run-up, it has since underperformed the broader index by over 20%, leaving passive investors as "bag holders" while early insiders took their gains.

Exaggerated Margins in a Dangerous Market Phase

The SpaceX IPO arrives in a context of historically exaggerated market margins. The 94x 2025 revenue valuation (or over 60x even using the most optimistic 2026 projections) far exceeds multiples markets have tolerated in the past: Facebook debuted at 11x sales (already considered extreme in 2012), while Google traded at 5-6x. It's a multiple higher even than Palantir, currently the highest-valued company in the S&P 500.

This market phase exhibits tech bubble characteristics:

-

Price-to-fundamentals decoupling: SpaceX's enterprise value/sales ratio has decoupled tenfold from big tech historical averages

-

Dominant profitability narrative: Selective EBITDA use ($8 billion claimed) hides crucial costs like satellite replacement (5-year lifespan) and Starship R&D investments, rendering real profits illusory

-

Contracting liquidity environment: VC funds that fueled the AI boom face a "liquidity plateau" and pressure to return capital to investors

The entire tech sector experienced a 30% correction between September 2025 and February 2026, with the North American Tech Software Index down 24% year-to-date by late February, driven by fears that "agentic" AI tools (like Anthropic's Claude) will obsolete traditional SaaS models. In this context, the SpaceX IPO represents a stress test for market capacity to absorb new offerings at sky-high valuations.

Systemic risk is evident: if SpaceX, with its combination of corporate astrology, questionable governance (Musk negotiating "with himself" to set valuations), and structural index manipulation, manages to sustain these prices, it will pave the way for a new era of passive bubble where index funds become forced buyers of artificially inflated stocks. If it fails, contagion risk to already fragile tech markets could be significant.

The Final Frontier or the Precipice?

SpaceX remains an extraordinary engineering success. However, as a public investment, the price paid for expected growth will matter. If the valuation is based on "comic book heroic assumptions" about capturing a billion customers who either already have better internet access or cannot afford the service, the "final frontier" for investors may prove to be a long way down.

The planetary alignment of June 2026 will undoubtedly be spectacular in the sky. What remains to be seen is whether it represents the dawn of a new era for the space industry, or the moment of maximum irrational exuberance before a painful realignment with the laws — not only of astronomy, but of financial gravity.

What's Your Reaction?